Industry News

Proposal to Include COVID-19 Claims in EMR Calculation is Denied

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

It appears the COVID-19 pandemic has finally entered an endemic stage and most companies have fully re-opened and/or are offering their employees some type of a hybrid work schedule. With this being the case, the California Workers’ Compensation Insurance Rating Bureau (WCIRB) proposed to amend the rule that excludes COVID-19 claims from the calculation of experience modifications for only claims with incident dates from December 1, 2019 through August 31, 2022.

Author, Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

It appears the COVID-19 pandemic has finally entered an endemic stage and most companies have fully re-opened and/or are offering their employees some type of a hybrid work schedule. With this being the case, the California Workers’ Compensation Insurance Rating Bureau (WCIRB) proposed to amend the rule that excludes COVID-19 claims from the calculation of experience modifications for only claims with incident dates from December 1, 2019 through August 31, 2022. In addition, the WCIRB proposed that effective September 1, 2022, any new COVID-19 claims occurring after this date would be factored into the calculation of an employer’s experience modification rate.

The WCIRB’s rationale for this recommendation was that current circumstances have greatly changed since the rule to exclude COVID-19 claims from the experience rating were initially adopted in 2020. COVID-19 is no longer a temporary short-term phenomenon and the risk of infection will be present in the general population for the foreseeable future.

With workplace safety standards in place, personal protective equipment and vaccinations available, employers who are diligent in protecting their employees would in turn have a lower experience modification than less safety-conscious employers in the same industry.

Fortunately, in late June 2022, this change was not approved by Commissioner Lara, but employers should still actively try to prevent the spread of COVID-19 within the workplace by having a written COVID-19 prevention program in place and follow the requirements set by the state and local health department.

While employers don’t have to worry that COVID-19 cases will affect their experience modification rate, they should still be concerned about the effects on their employees and bottom line. Having employees miss work because of COVID-19 puts extra strain on other employees and can effect productivity, and thus profitability.

Rancho Mesa has updated its COVID-19 Prevention Program Template designed for California businesses. Request your COVID-19 Prevention Plan template online or contact me at sclayton@ranchomesa.com or (619)937-0167.

Dashboard Spotlight: Your Path to an Experience MOD Below 1.00

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

Rancho Mesa’s Safety KPI Dashboard allows businesses the ability to clearly visualize their path to an Experience MOD (XMOD) below 1.00 through goal setting.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

Rancho Mesa’s Safety KPI Dashboard allows businesses the ability to clearly visualize their path to an Experience MOD (XMOD) below 1.00 through goal setting.

In order to set your business goal, you will need to use three available metrics from your custom dashboard.

Lowest Possible XMOD – This is the best case scenario if you had zero claims for the three-year XMOD period.

Claim Cost Per 1 XMOD Point – This is the amount of incurred claim cost that impacts your XMOD by 1 point.

Unit Stat Date – This is the moment when your information is sent to the rating bureau for next year’s XMOD to be calculated.

Using these three metrics together, you can effectively set your goal and manage your XMOD accordingly.

The XMOD is calculated using a running three-year window of the most recently completed workers’ compensation policies. Each policy period will contribute a set amount of weight on the XMOD calculation based on payroll and claims.

Take your lowest possible XMOD from the KPI dashboard and subtract that number from .99.

You will be left with the amount of XMOD points your company can absorb while still keeping your XMOD below 1.00.

Divide that number by three and you can evenly distribute the amount of XMOD points you can have each year to keep your XMOD below 1.00.

Take the annual XMOD points and multiple by your Claim Cost Per 1 XMOD Point.** This will give you the maximum claim cost available per policy period.

Example:

Lowest Possible XMOD: 47

Claim Cost Per 1 XMOD Point: $3,100

Unit Stat: September 30th

(.99) – (.47) = .52 (Number of XMOD points available to absorb and keep XMOD below 1.00)

(.52) / (3) = 17.3 (Max XMOD points per year)

(17.3) * (3,100) = $53,630 (Max claim cost available per policy period) **

**Must consider your primary threshold, which is also a number available on the KPI Dashboard.

Knowing these numbers, along with when your unit stat date comes up, allows you to strategically plan.

If all of this seems complicated or you just want to see what your company’s dashboard would look like, request a personalized KPI Dashboard and we can discuss how you can develop a path to an XMOD below 1.00.

Work-Related Automobile Accidents and Their Correlation With Workers’ Compensation Claims

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

In California, motor vehicle accidents are among the leading cause of severe injuries on a daily basis. From a risk management perspective, a company’s fleet safety program has a primary goal of keeping employees safe while driving which lowers the amount of annual auto premiums paid.

Author, Kevin Howard, Account Executive, Rancho Mesa Insurance Services, Inc.

In California, motor vehicle accidents are among the leading cause of severe injuries on a daily basis. From a risk management perspective, a company’s fleet safety program has a primary goal of keeping employees safe while driving which lowers the amount of annual auto premiums paid.

What is not typically discussed when talking about fleet safety is the impact a work-related auto incident has on a workers’ compensation policy and experience modification. This article will discuss some of those impacts.

EXPERIENCE MODIFICATION IMPACT

When broken down, workers’ compensation premiums are driven by many factors. A main factor for pricing is the experience modification. Experience modifications are a measure of safety for a company when compared to others in the same field. Workers’ compensation claims adversely affect experience modifications.

Typically, business owners invest time, energy and resources into their safety program in the form of personal protective equipment (PPE), stretching before labor, tailgate meetings and job hazard analysis. But, the “big claim” businesses are doing so much to avoid could come from an auto incident. A heavy dose of fleet safety training should be mixed into the safety topic agenda, tailgate meetings and discussions regarding minimal driving record requirements for employees to drive on behalf of a company.

Businesses in California are required to offer no-fault workers’ compensation insurance which means it doesn’t matter who is at fault, the injury will be covered by a worker’s compensation carrier.

When a work-related auto accident occurs and there is an injury involved with an employee, the experience modification will be affected adversely based on the incurred cost of the claim as well as the loss ratios.

SUBROGATION

If another party is at fault regarding a workers’ compensation claim, the insurance carrier who is tending to the claim can subrogate and try to recoup the paid amount from the responsible party.

The issue workers’ compensation carriers deal with regarding subrogating auto claims is that the California minimum required auto liability limit is only $5,000. This amount would not cover most injuries suffered by an employee in an auto accident. Also, there is a high percentage of drivers who are uninsured which makes subrogation impossible in a claim scenario.

Overall, subrogation is pretty difficult in this specific area of workers’ compensation. The best defense is to avoid auto incidents as much as possible.

MULTIPLE EMPLOYEE IN ONE VEHICLE

Especially with gas prices soaring, carpooling to jobsites can be a popular method of getting employees from one location to the next. Regardless of fault, this could create multiple workers’ compensation injuries at once. Multiple workers’ compensation claims will adversely affect experience modifications, loss ratios and DART rates.

These factors should be considered when creating a car pool scenario for employees travel from jobsite to jobsite.

Important factors to consider if you do utilize carpooling to jobsites could be:

Does the driver meet out company standards with his or her driving record?

Is the vehicle’s maintenance up to date? (e.g., tires, windshield wipers, etc.)

Are there multiple high wage earners traveling in the same vehicle?

TEMPORARY DISIBILITY COST ON THE RISE

With a major labor shortage occurring in California, wages have risen in order to attract and retain labor and highly qualified employees. A severe motor vehicle accident which creates a worker’s compensation claim could adversely affect an employer’s experience modification because two-thirds of the amount of the injured workers’ pay is a larger dollar amount on average than it has been in the past.

This could create a larger claim because of the amount of temporary disability being paid while an employee is hospitalized or unable to come back to work with or without restrictions.

FLEET SAFTEY CONTROLS

When budgeting for an overall safety program, business owners should factor in the multitude of impacts that an auto claim can have on a business. Controls like GPS/telematics, drug testing kits, MVR pull programs, and vehicle maintenance programs are examples of investing in fleet safety.

Fleet safety programs can save lives, save money and can create a stronger culture of safety throughout a business.

Rancho Mesa’s Risk Management Center has a searchable safety library with fleet safety materials that can be used to train employees. Register online for Rancho Mesa’s Fleet Safety webinar on May 26, 2022 from 9:00 am PDT – 10:00 am PDT. Or, contact me at khoward@ranchomesa.com or (619) 438-6874 if you have questions about your auto policy.

Actual Impact of Auto Claims to Your Bottom Line?

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

In two previous articles/podcasts, we explored “below the surface” impacts from payroll inflation and lost time workers’ compensation claims. We provided detail on how these can negatively impact a business’s productivity and profitability and what companies can do to mitigate those impacts. Today, let’s look at another area where you need a keen awareness to really understand all the impacts.

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

In two previous articles/podcasts, we explored “below the surface” impacts from payroll inflation and lost time workers’ compensation claims. We provided detail on how these can negatively impact a business’s productivity and profitability and what companies can do to mitigate those impacts. Today, let’s look at another area where you need a keen awareness to really understand all the impacts.

What is the true impact an auto accident can have on areas of your business? For discussion, let’s consider an accident where your driver is at fault and also injured. This type of accident is much like an octopus in that it is going to touch many areas of your insurance program.

First, there is the damage to your auto, obviously this will be covered under the physical damage portion of your policy.

Second, you will have the physical damage and potential bodily injury to the third party whom your driver hit. This would fall under the auto liability portion of your policy. Additionally, if the other party or parties are severely injured it could penetrate your initial layer of liability insurance requiring your umbrella/excess policy to respond. As a side note, in my 35 years in the insurance industry, the largest claims that we see are predominately in auto due to the potential of severe bodily injury.

Third, given that your driver was injured, this claim will trigger your workers compensation policy to provide coverage for both the indemnity and medical costs of their injuries.

Fourth, the claims will impact your loss ratios in both your automobile insurance and workers compensation, causing the potential for future premium increases.

Fifth, this claim will also cause your Experience Modification to rise, which again will cause the potential for future premium increases as well as potentially, if you’re a contractor, eliminate you from bidding on certain work.

Sixth, replacing the injured driver may mean having to hire someone new which will increase payroll and lead to additional training time and a loss of productivity.

I’m sure your head is spinning and you’re probably wondering “all this, from one accident?” What should I do? Thankfully there are several things you can do to mitigate this before the accident occurs. Consider the following:

Do you have a formal fleet safety program in place? If not, work with your trusted advisor to get one in place. If you would like us to help you with that contact our client services team to set up a time to review our trainings and fleet safety resources with you.

Do you have a distracted driving policy in place for your drivers? This is by far the leading cause of auto accidents and while many are at low speeds, they can still be very costly. High speed distracted driving accidents can be catastrophic.

Are you participating in the DMV Pull Program? If not, this is a valuable tool that will provide you with information on your drivers’ experience regardless if the infraction or incident occurred as a part of work or outside of work. Most auto insurance carriers will view this as a subjective credit on your premium rating. You can do this very inexpensively and direct via the DMV website.

Are you using any telematics tools, like GPS, speed and breaking tracking, cameras (both forward facing and rear facing)? These devices are again viewed as a subjective credit by insurance carriers.

Once an accident occurs, are you completing a thorough accident investigation report with a description of the accident, witness statements, pictures, police report (if available) and then reviewing the data to determine root cause and possible changes to your fleet safety program?

As you’ve seen, the key to mitigating this type of claim is to keep it from occurring, which is easier said than done. Accidents will still happen. While you may not be the “at fault’ party in many of the accidents, reducing the likelihood of your driver being at fault starts with your commitment to a strong fleet safety program. If you need help in creating this fleet safety program, please contact our client services team to get started.

Once you have a strong program in place and you feel more in control of your vehicle safety performance there are other cost saving programs that you would be eligible to consider. We discussed those in other articles where we explore Performance Based Insurance Programs.

I hope you find this information useful and that you are able to take away an idea or two that might improve your operations. To learn more best practice techniques, contact us or reach out to me directly at dgarcia@ranchomesa.com.

How Higher Average Pay Can Lead to Work Comp Savings

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Wage thresholds have increased consistently in the past decade. This has pushed owners to give sizable raises every few years to maximize employee compensation, but also reducing insurance cost. The experience modification (MOD) and payrolls are key factors in developing a company’s net rates for workers’ compensation, but average wage per hour represents a big differentiator for most carriers and can lead to even more savings.

Author, Casey Craig, Account Executive, Rancho Mesa Insurance Services, Inc.

Wage thresholds have increased consistently in the past decade. This has pushed owners to give sizable raises every few years to maximize employee compensation, but also reducing insurance cost. The experience modification (XMOD) and payrolls are key factors in developing a company’s net rates for workers’ compensation, but average wage per hour represents a big differentiator for most carriers and can lead to even more savings.

Paying your most competent employees above the wage threshold leads to less fraudulent claims, longer tenured employees, and a happier workplace, not to mention the benefit of a drastic cut in net rates for that class code. The gap that is sometimes felt is when there are employees that have the same job description and are earning 30-40% less. Managing payroll inflation is always critical for businesses but let’s think about what this can do to the employees bringing the average pay down for your company. Consider:

More fraudulent claims as the employee has less to lose if they are terminated or laid off;

Resentment toward employees that are doing same job but making more;

Employees are more likely to move to another company to get raises;

Likelihood to miss more time when injured, leading toward higher temporary disability pay which typically can lead to a higher XMOD.

Insurance companies and their underwriters look closely at average salary per employee when they receive a submission with the renewal documentation.

The higher the average pay, the more aggressive they can be with potential scheduled credits in most cases. Obviously, the employer must be selective with who receives a raise and how much but also understand what potentially positive impacts there can be when giving raises in order to hit those thresholds.

And, perhaps just as important is partnering with a broker that specializes in your industry and knows how to properly benchmark you with like organizations. This consistently leads to more productive discussions with underwriters that lead to more scheduled credits. The happier your workforce is, the less claims you tend to see and that translates to long-term savings.

If you have any questions about how you compare to your industry or would like to discuss any other insurance related topic, do not hesitate to reach out to 619-937-0164 or email me directly at ccraig@ranchomesa.com.

Experience Mod KPI Provides Trend Analysis, Opportunity Assessment, and Vital Management Tools

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

In January 2021, we launched the Safety Key Performance Indicator (KPI) Dashboard to provide a tool for our customers to use as a bridge between their experience mod and safety performance.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

In January 2021, we launched the Safety Key Performance Indicator (KPI) Dashboard to provide a tool for our customers to use as a bridge between their experience mod and safety performance.

Our primary goals were to:

Eliminate surprises

Simplify concepts

Track performance

Highlight the positive and negative trends

Benchmark safety performance against industry competitors

An experience mod above 100 can limit a landscape company’s ability to be awarded jobs or maintain contracts, increase insurance premiums, and have other significant financial implications.

Our dashboard is a tool companies can use to strategically manage the underlying components that directly impact the experience mod and help project future experience mod deviations. Rancho Mesa can help interpret the results and provide insights to help improve your performance.

Not a Rancho Mesa client but interested in seeing what your dashboard looks like? Complete our new KPI Dashboard quick form, to see how your company measures up.

California’s Landscape Industry Prepares for Ex-Mod Changes

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

For the first time in several years the Expected Loss Rate for class code 0042 has increased from $2.38 to $2.42, a 2% increase.

Bottom line, although very minimal, this should help bring the experience mod down.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

For the first time in several years the Expected Loss Rate for class code 0042 has increased from $2.38 to $2.42, a 2% increase.

Bottom line, although very minimal, this should help bring the experience mod down.

This information will impact any landscape company who has a policy effective date of September 1, 2021 and beyond.

Based on a couple of projection comparisons, we have seen an impact of 1 to 4 points come off the experience mod for landscape companies.

Landscape companies working with Rancho Mesa with policy effective dates after 9/1/2021 will see updated information on their KPI Dashboard, at the next review.

For landscape companies not working with Rancho Mesa, you can request a custom KPI Dashboard today by reaching out to Drew Garcia.

How to Choose a Workers’ Compensation Carrier Partner

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

Many years ago, when I was a young producer, one workers’ compensation carrier legend pulled me aside and told me never to forget that a workers’ compensation decision is not a one-year decision, but at least a 4-year decision. Of course, policies are only written on a one-year basis but what he was teaching me was that the carrier you choose will handle all the claims you have through your Experience Modification cycle. So, evaluating and recommending a workers’ compensation partner for my clients just became a much more thorough analysis of many critical factors beyond just the premium.

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

Many years ago, when I was a young producer, one workers’ compensation carrier legend pulled me aside and told me never to forget that a workers’ compensation decision is not a one-year decision, but at least a 4-year decision. Of course, policies are only written on a one-year basis but what he was teaching me was that the carrier you choose will handle all the claims you have through your Experience Modification cycle. So, evaluating and recommending a workers’ compensation partner for my clients just became a much more thorough analysis of many critical factors beyond just the premium.

I understand and want to acknowledge that competitive pricing is very important, yet other than price, most business owners are not sure what to look for when comparing carriers. All businesses should consider the following in their evaluation of a workers’ compensation carrier:

What is the A.M. Best rating of the carrier?

How long have they been in the State workers’ compensation marketplace?

What is their premium volume within the State?

What “in-house” services does the carrier provide? Two services for special consideration are:

The Claims Department

Loss Control Service

How does their medical cost containment numbers compare to the industry averages?

How does their claim closing rates compare to the industry average?

Are the following services available?

Telemedicine

Nurse Triage

For any businesses that pay above $250,000 in annual premium, should consider these additional questions:

Does the carrier offer a dedicated indemnity claims examiner for your business?

Does the carrier offer Claim Review Meetings?

Does the carrier offer a Client Services coordinator?

Does the carrier offer on-line claim status information?

What loss sensitive programs do they offer?

Further, for any businesses that are exploring loss sensitive programs (usually above $400,000 in annual premium) like deductible workers’ compensation, they should evaluate the following:

What are the terms of the letter of credit required?

Is there a Loss Conversion Factor (LCF)?

Is a Loss Fund required?

How are Allocated Loss Adjustment Expenses (ALAE) handled?

Is there a policy deductible aggregate?

Are there any claims handling charges?

Are there Medical Cost Containment charges?

Since many of the concepts and terms above require a deeper understanding and explanation, listen to my podcast episodes where I examine this topic in greater detail.

Also, consider attending one or both of my live webinars that cover this topic and afford you the opportunity to ask questions. Register for our Thursday April 1, 2021 webinar where I will focus on businesses with annual premiums below $400,000, and/or register for my Thursday April 8, 2021, webinar where I will deal specifically with deductible workers’ compensation. Both webinars will be 30 minutes in length.

If you would prefer to speak with me directly, I can be reached at (619) 937-0170 or email me at dgarcia@ranchomesa.com.

I wish you all a safe and profitable 2021.

California’s Workers’ Compensation Landscape May Reach a Valley in Coming Year

Author, Drew Garcia, Vice President of the Landscape Group, Rancho Mesa Insurance Services, Inc.

The workers’ compensation market for landscape companies in California has remained in a downward trend since 2015. As a result, landscape business owners have realized lower rates and subsequently aggressive premiums. The following are some key insights to help landscape businesses prepare for their 2021 workers’ compensation insurance renewal.

Author, Drew Garcia, Vice President of the Landscape Group, Rancho Mesa Insurance Services, Inc.

The workers’ compensation market for landscape companies in California has remained in a downward trend since 2015. As a result, landscape business owners have realized lower rates and subsequently aggressive premiums.

The following are some key insights to help landscape businesses prepare for their 2021 workers’ compensation insurance renewal.

For Experience MOD (XMOD) purposes, it’s important to know the Expected Loss Rate (ELR) for the landscape class code (0042) has decreased 8% over last year, $2.38 per $100. With a lower ELR comes an adverse effect for landscape companies’ individual XMOD, as a result of lower expected losses. Lower ELRs also drive down the primary threshold, amplifying each claim’s impact on the XMOD. Have your 2021 XMOD projected early to identify any possible implications.

Pure premium rates are developed by the Workers' Compensation Insurance Rating Bureau of California (WCIRB) and approved by the insurance commissioner to reflect the expected losses and loss adjustment expenses for each class code. Insurance carriers can then use these rates to come up with their own base rates to establish premiums. Pure premium for the landscape industry is down 8% over last year, from $5.61 to $5.14. The WCIRB also added a $.06 surcharge for COVID-19 claim impacts for the landscape industry. The Landscape Industry was labeled under tier 3 of 5, were the $.06 surcharge will be applied. Other tiers such as 4, 5, and 6 saw $.012, $.18, and $.20 surcharges as it was deemed those industries have a larger exposure share to COVID claims. In the end, with the surcharge, Pure Premium is slightly down and theoretically should lower carrier base rates.

Watch a 10-minute webinar where Drew Garcia explains the California Workers' Compensation marketplace for the landscape industry.

Areas like Los Angeles Country, Riverside County, and San Bernardino Country have had higher claims activity and claim outcomes than other parts of the state. Carriers use territory factors to more accurately align their premium for your business, depending on your location. Territory factors can either credit or debit your policy based on the location of your business or surrounding areas where you operate. For example, if you are a landscape company in Riverside County but doing business in San Diego Country, make sure you are breaking out these operations so your underwriter can accurately evaluate the correct percentage of operations in Riverside vs. San Diego.

The average base rate filed by insurance carriers for class code 0042 is $10.63, which is down 7% over last year. Carriers determine base rates based on industry appetite, historical loss experience, pure premium rates, and overhead. Not all carriers have an appetite for landscape business and the lowest base rate does not mean the lowest net rate. Insurance carriers have the ability to apply “schedule rating” which is a list of criteria they file for with the California Department of Insurance to allow underwriters the ability to deviate off the price.

In 2019, the top three carriers writing workers’ compensation insurance in California by premium volume was State Fund (10.56%), Berkshire Hathaway Homestate Companies (7.12%), and Insurance Company of the West (6.94%). Rounding out the top ten were Hartford, Travelers, AmTrust, Zurich, Chubb, Fairfax, and Employers.

Our advice for 2021:

Have your companies 2021 XMOD projected today, if not at least 6 months before your policy is set to renew.

Meet with your insurance professional 120 days before renewal to determine the renewal strategy.

If you are discussing different carrier options with your agent, ask the next level questions:

What other landscape companies does this carrier work with?

What is their rating?

How long have they written workers’ compensation in California?

Are claims handled in house or by a third party?

The numbers above indicate the perpetuation of a soft market, however, we are steadily seeing the delta of decrease shorten. Take this information to help your company formulate your renewal strategy and impact the discussions you have with your insurance agent in 2021.

If you have questions about your workers’ compensation renewal, contact me at (619) 937-0200 or drewgarcia@ranhcomesa.com.

Post COVID-19 XMODs Threaten a Double Whammy

Author, Kevin Howard, C.R.I.S., Account Executive, Rancho Mesa Insurance Services, Inc.

COVID-19 has created a multitude of challenges for California business owners in the first half of 2020. A concerning trend is the potential combination of lower payrolls and the California Workers’ Compensation Insurance Rating Bureau’s (WCIRB) recommendation to lower expected loss rates, creating what very likely could be significant Experience Modification Rate (XMOD) increases for numerous California businesses.

Author, Kevin Howard, C.R.I.S., Account Executive, Rancho Mesa Insurance Services, Inc.

COVID-19 has created a multitude of challenges for California business owners in the first half of 2020. A concerning trend is the potential combination of lower payrolls and the California Workers’ Compensation Insurance Rating Bureau’s (WCIRB) recommendation to lower expected loss rates, creating what very likely could be significant Experience Modification Rate (XMOD) increases for numerous California businesses.

Whammy #1 - Lower Payrolls

With the economy screeching to a halt in March of this year due to the shelter in place restrictions, payrolls and employee counts have been dramatically reduced. Since the XMOD calculation is based on a rolling three years of payroll and claims, should the year dropping out of the calculation have larger payrolls than the year entering and assuming the same claim amounts for each year, the XMOD would increase.

Whammy #2 – Lower Expected Loss Rates (ELR)

ELRs are the factors used to anticipate a class code’s claim cost per $100 for the experience rating period. Stated simply, it’s a rate per, $100 of payroll by class code that projects the claim amounts the WCIRB believes should occur for that class code. Thus, should ELRs decrease; it would have the effect, given no change in the claims, of raising the XMOD.

California businesses should pay close attention to their individual ELRs as the WCIRB annually recommends updated rates during their June regulatory filing period. The 2021 rates were recently proposed on June 25, 2020 by the WCIRB and will be waiting approval in September by Insurance Commissioner Ricardo Lara.

Below is a breakdown of the 2021 proposed ELRs by class code with notable double digit increases highlighted:

2021 Proposed ELRs

| Class Code | 2020 ELRs | 2021 Proposed ELRs | Increase/Decrease % |

|---|---|---|---|

| 3724 Solar/Millwright | 1.74 | 1.81 | 4% |

| 5187 Plumbing > $28 | 1.18 | 1.13 | -4% |

| 5183 Plumbing < $28 | 2.6 | 2.6 | 0% |

| 5542 Sheet Metal > $27 | 1.4 | 1.35 | -3% |

| 5538 Sheet Metal < $27 | 2.3 | 2.39 | -12% |

| 6258 Foundation Prep | 2.65 | 2.48 | 2% |

| 0042 Landscape Gardening | 2.59 | 2.38 | -8% |

| 0106 Tree Pruning | 3.91 | 4.11 | 5% |

| 5140 Electrical Wiring > $23 | 0.81 | 0.73 | -10% |

| 5190 Electrical Wiring < $23 | 1.89 | 1.82 | -4% |

| 5470 Glaziers > $33 | 1.63 | 1.81 | 11% |

| 5467 Glaziers < $33 | 4.3 | 3.81 | -11% |

| 5028 Masonry > $28 | 2.17 | 2.13 | -1.8% |

| 5027 Masonry < $28 | 4.73 | 4.03 | -14% |

| 5482 Painting/ Waterproofing > $28 | 1.42 | 1.57 | 10% |

| 5474 Painting/ Waterproofing < $28 | 3.68 | 4.08 | 10% |

| 5186 Automatic Sprinkler Install > $29 | 1.11 | 1.14 | 3% |

| 5185 Automatic Sprinkler Install < $29 | 2.45 | 2.2 | -10% |

| 5205 Concrete/Cement work > $28 | 1.95 | 1.71 | -12% |

| 5201 Concrete/Cement work < $28 | 3.95 | 3.45 | -12% |

| 5432 Carpentry > $35 | 2.01 | 2.05 | 2% |

| 5403 Carpentry < $35 | 5.27 | 4.91 | -7% |

| 5447 Wallboard Application > $36 | 1.34 | 1.14 | -14% |

| 5446 Wallboard Application < $36 | 2.76 | 2.67 | -3% |

| 5485 Plastering or Stucco >$32 | 2.66 | 2.55 | -4% |

| 5484 Plastering or Stucco < $32 | 4.78 | 4.41 | -8% |

| 5443 Lathing | 2.37 | 2.23 | -6% |

| 5553 Roofing > $27 | 3.9 | 3.89 | -2% |

| 5552 Roofing < $27 | 9.85 | 9.23 | -6% |

| 6220 Excavation/Grading > $34 | 1.24 | 1.08 | -12% |

| 6218 Excavation/Grading < $34 | 2.34 | 2.59 | 10% |

| 5436 Hardwood Flooring | 2.03 | 2.01 | -1% |

| 3066 Sheet Metal Prod Mfg. | 1.94 | 2.00 | 3% |

| 8018 Stores - Wholesale | 2.67 | 2.81 | 5% |

| 8804 Shelter/Social Rehab | 1.25 | 1.30 | 4% |

| 8827 Hospice and Homecare | 1.72 | 1.54 | -10% |

| 9059 Childcare | 0.99 | 1.07 | 8% |

| 8834 Physicians | 0.34 | 0.34 | 0% |

| 8868 Colleges/ Professors Private-Teachers | 0.36 | 0.37 | 3% |

| 9101 Colleges/Schools Private-Other | 2.50 | 2.13 | -14% |

Should Commissioner Lara approve the ELR changes in September, a majority of class codes will be seeing a decrease which can lead to higher XMOD’s in many cases. That possibility, combined with lower incoming payrolls, requires proactive risk mitigation, claim management and detailed planning with your broker.

If you are seeking a partner with the tools to address these needs, please reach out to Kevin Howard at Rancho Mesa Insurance Services, Inc. at (619) 438-6874.

Landscape Companies with Low Experience MODs Do These 5 Things

Author, Drew Garcia, Vice President of the Landscape Group, Rancho Mesa Insurance Services, Inc.

Landscape companies with a low Experience Modification Rating (XMOD/EMR) typically exhibit similar best practices when dealing with work-related injuries. Their proactive approach helps close claims faster and return employees to work sooner than their counterparts.

Author, Drew Garcia, Vice President of the Landscape Group, Rancho Mesa Insurance Services, Inc.

Landscape companies with a low Experience Modification Rating (XMOD/EMR) typically exhibit similar best practices when dealing with work-related injuries. Their proactive approach helps close claims faster and return employees to work sooner than their counterparts.

The XMOD/EMR is a unique number assigned to a business that is made up of their historical loss figures and audited payroll information vs. the same information for companies involved in the company’s same industry. Generally, if your business has experienced more claim activity than the industry average, you will have a XMOD/EMR above 1.00. The opposite is true; if you have had less claim activity, your XMOD/EMR will be below 1.00. The XMOD/EMR impacts the rates you pay for workers’ compensation by crediting (XMOD/EMR below 1.00) or applying a surcharge (XMOD/EMR above 1.00).

Here are the 5 best practices used by landscape companies who have an XMOD/EMR) below 1.00.

1. An Aggressive Return to Work Program

If you heard our podcast episode with Roscoe Klausing of Klausing Group, you will hear him coin the phrase an “aggressive return to work program” which was a key component to his company, of more than 70 employees, going 3 years without a lost time accident.

Aggressively finding a way to help bring an injured employee back on modified work restrictions has long been proven to provide positive outcomes for everyone involved. Benefits of bringing an employee back on modified duties include:

Eliminating temporary disability payments from the claim cost.

Lower the dollar amount of medical treatments.

Reduce the overall cost of the claim.

Lower the potential impact the claim would have on your XMOD/EMR.

Improve injured employee morale.

2. Timely Reporting and Accident Detail

It is critical to constantly remind your front line supervisors and employees that they must report all injuries no matter the severity as soon as possible. Studies have shown that work related injuries reported with the first 5 days have a dramatically lower average claim cost and litigation rates than those reported after 5 days.

Two measurable statistics for you to keep an eye on are:

The lag time between when an injury is reported to you from an employee.

The amount of time it takes you to report this information to your insurance carrier.

By conducting a thorough accident investigation at the time of injury and providing a report to your insurance claim professional, you will speed up the claims process and lower costs. Eliminating the time delays caused by the claim professional waiting for details or additional information is critical in making sure your injured employee is on the fast track to recovery. To assist the landscape industry in completing this necessary step, Rancho Mesa has created a free, fillable, carrier approved accident investigation report for use by the landscape industry.

3. Communication

Keeping in constant communication with employees who are injured is vital to a positive outcome. At times, the workers’ compensation process can seem slow. Some injuries will take longer than others. This can lead injured employees to feel frustrated and uncertain. Make sure you are addressing their concerns and checking in on them, frequently.

4. Know the Basic Principles Behind the XMOD/EMR

You do not need to know the XMOD/EMR formula, but you should have an understanding of the basic concepts that leads to XMOD/EMR inflation.

You should know when your claim information will be sent to your rating bureau for next year’s XMOD/EMR calculation and make sure you are familiar with the status of each claim before the information is locked.

If your rating bureau uses a Primary Threshold or Split Point, it is good to understand how this number impacts claim cost and each claim’s impact on the XMOD/EMR.

Know your lowest possible XMOD/EMR, this would be all your payroll with zero claims. The points between your lowest possible XMOD/EMR and your current XMOD/EMR are the controllable points.

Know the policy years that are used to calculate the XMOD/EMR.

5. Relationship With Your Carrier and Claims Professional

The carrier claims professional who handles your injuries can have a huge impact on the outcome of the claim. If you are fortunate enough to have a dedicated claim adjuster assigned to your company, make it a point to call and introduce yourself before the first claim occurs. The adjuster should have a very good understanding of:

Your attitude and policy regarding return to work programs.

The level of accident information they will receive from you.

Who will be your company’s main contact throughout the claim process?

Consider these five best practices when handling your workers’ compensation claims to keep your XMOD/EMR under control and your workers’ compensation costs low.

Work Comp Unit Stat: The Meeting That Saves You Money

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

California business owners are aware that their experience modifier (XMOD) is published annually, roughly three to four months before the expiration of their current workers compensation policy term. However, more often than not, companies are missing an incredible opportunity to make an impact on the calculation of their XMOD by strategically evaluating their work comp claims prior to the most critical month in the XMOD calendar known as Unit Stat.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

California business owners are aware that their experience modifier (XMOD) is published annually, roughly three to four months before the expiration of their current workers compensation policy term. However, more often than not, companies are missing an incredible opportunity to make an impact on the calculation of their XMOD by strategically evaluating their work comp claims prior to the most critical month in the XMOD calendar known as Unit Stat.

The Workers’ Compensation Insurance Rating Bureau (WCIRB) defines the process of receiving loss and payroll information by classification as the Unit Statistical Report. The information is reported to the WCIRB by insurance carriers at specific intervals based on your company’s policy effective date. The information is valued for the first time 18 months after the inception of your policy and every 12 months thereafter.

A policy that incepts in January 2020 will be valued for the first time in July of 2021 (18 month mark). This information will remain in your XMOD calculation for the valuations at 30 months and 42 months.

Once this information has been received by the WCIRB, from the respective carriers, it cannot be altered or changed until the following year’s unit stat. Thus, you may have a positive outcome on an existing open claim (reserve reduction or closure) but not see the benefit until the following year. Revisions to the XMOD once published are limited to a few circumstances; more information about revisions can be found here.

The loss information, sent to the WCIRB from the insurance carriers, will be evaluated at the paid (closed claim) or reserved (open claim) amounts. Typically, a claim that has been open for longer than 18 months signifies severity, litigation, lost time, permanent disability, or a combination of the group. For this reason it is absolutely critical that as a part of your risk management process you execute a

pre-unit stat meeting.

When should I schedule my Unit Stat meeting?

What should I do at this meeting?

Who needs to be involved?

How will this meeting save me money?

As a client of Rancho Mesa, we build this meeting into your annual service plan and take care of engaging the parties who need to be involved for the betterment of your XMOD.

Ready to learn more about Unit Stat? Join us for a complimentary 25-minute webinar where we will discuss the process in greater detail and take time for Q&A.

Still not sure if further learning is necessary, ask yourself these questions:

Have you ever been surprised by your XMOD being higher than you would have thought?

Have you ever had an XMOD above 1.00?

Has your XMOD ever caused your premium to increase?

The webinar can be viewed on-demand by clicking the link below.

Contractors Brace for Impact of 2020 Expected Loss Rates

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

California contractors focused on their experience modification are paying close attention to the soon to be published 2020 Expected Loss Rates (ELRs).

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

California contractors focused on their experience modification are paying close attention to the soon to be published 2020 Expected Loss Rates (ELRs).

ELRs determine the expected claim cost per $100 in pay roll for each class code during an Experience Modification (Ex-Mod) period. These rates are updated annually. The 2020 rates were recently approved on September 5, 2019. Changes in each specific class code’s ELR can positively or negatively impact a contractor’s Ex-Mod calculation.

In a nutshell, if an expected loss rate drops from one year to another with no material changes to payroll or claims, Ex-Mod’s will increase. Additionally, if an expected loss rate increases, Ex-Mod’s will decrease using the same example.

Below is a breakdown of the 2020 ELRs per class code with notable double digit increases highlighted:

| Class Code | 2020 ELR | Increase/Decrease % |

|---|---|---|

| 3724 Solar/ Millwright | 1.74 | -4% |

| 5187 Plumbing > $28 | 1.18 | -8% |

| 5183 Plumbing < $28 | 2.6 | -5% |

| 5542 Sheet Metal > $27 | 1.40 | -4% |

| 5538 Sheet Metal < $27 | 2.30 | -12% |

| 6258 Foundation Prep | 2.65 | -3% |

| 0042 Landscape Gardening | 2.59 | -15% |

| 0106 Tree Pruning | 3.91 | -21% |

| 5140 Electrical Wiring > $23 | .81 | -6% |

| 5190 Electrical Wiring < $23 | 1.89 | +2% |

| 5470 Glaziers > $33 | 1.63 | +7% |

| 5467 Glaziers < $33 | 4.30 | -2% |

| 5028 Masonry > $28 | 2.17 | -9% |

| 5027 Masonry < $28 | 4.73 | -18% |

| 5482 Painting/ Waterproofing > $28 | 1.42 | -15% |

| 5474 Painting/ Waterproofing < $28 | 3.68 | -7% |

| 5186 Automatic Sprinkler Install > $29 | 1.11 | +5% |

| 5185 Automatic Sprinkler Install < $29 | 2.45 | -18% |

| 5205 Concrete/Cement work > $28 | 1.95 | -5% |

| 5201 Concrete/Cement work < $28 | 3.95 | -4% |

| 5432 Carpentry > $35 | 2.01 | -7% |

| 5403 Carpentry < $35 | 5.27 | -9% |

| 5447 Wallboard Application > $36 | 1.34 | -12% |

| 5446 Wallboard Application < $36 | 2.76 | -21% |

| 5485 Plastering or Stucco >$32 | 2.66 | -6% |

| 5484 Plastering or Stucco < $32 | 4.78 | -27% |

| 5443 Lathing | 2.37 | -18% |

| 5553 Roofing > $27 | 3.90 | -14% |

| 5552 Roofing < $27 | 9.85 | -4% |

| 6220 Excavation/Grading > $34 | 1.24 | -24% |

| 6218 Excavation/Grading < $34 | 2.34 | -5% |

The data above shows that a majority of class codes will be seeing a decrease in ELRs which will cause higher Ex-Mods in many cases. That reality creates a heightened need for loss control, claim management and post claim strategies. If you are seeking a partner with the tools to address these needs, please reach out to Rancho Mesa Insurance and our team of professionals at (619) 438-6874.

The Ticking Time Bomb for Plumbing and Mechanical Contractors: Lower Expected Loss Rates Can Mean Higher Experience Modifications

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

The Workers Compensation Insurance Rating Bureau (WCIRB) released the 2019 Expected Loss Rates (ELR’s) in the 4th quarter of 2018. The ELR’s in the plumbing class code 5187 dropped 17% on January 1st 2019. This decrease is not getting significant attention, but could potentially create negative implications for California plumbing contractors and their respective experience modifications in 2019, 2020 and beyond.

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

The Workers Compensation Insurance Rating Bureau (WCIRB) released the 2019 Expected Loss Rates (ELRs) in the 4th quarter of 2018. ELRs are the average rate at which losses for a classification are estimated to occur during an experience rating period. They are generally expressed as a ratio per $100 of payroll and can often have a dramatic impact on experience modifications. To support this point, the ELRs in the plumbing class code 5187 dropped 17% on January 1, 2019. This decrease is not getting significant attention, but could potentially create negative implications for California plumbing contractors and their respective experience modifications in 2019, 2020, and beyond. All plumbing and mechanical contractors should be made aware so they can prepare and make changes to protect themselves from the impact. Similar to a leak behind a wall, this could go undetected until the experience mods are released and then it is too late and too much damage has been done.

LINKING ELRs WITH YOUR PRIMARY THRESHOLD

The lowered expected loss rates also impact primary thresholds. Your primary threshold is the maximum primary loss value for each individual worker’s compensation claim. If primary thresholds move lower, one small lost time claim can cause a significant spike in an experience modification. An elevated experience modification can impact not only pricing, but opportunities to bid certain types of work within the commercial sector.

WHAT CAN YOU DO TO GET OUT IN FRONT OF THIS?

If these terms are completely new to you and your organization, lean on your insurance broker to provide the education needed to get up to speed. That can start with building a detailed service plan that focuses on controlling your experience modification. Some examples of critical elements that should be discussed would include:

Addressing open reserves on claims that are impacting the future experience modification.

How the timing of the unit stat filing will affect the future experience mod and cost.

Ensuring that your safety program addresses the root cause of claim frequency and severity.

Trainings that are aligned with OSHA compliance.

Experience MOD forecasting up to 7 months prior to your firm’s effective date.

AVOIDING THE TICKING TIME BOMB

The ticking time bomb can be avoided by taking certain steps and actions that are strategically put in place with your insurance broker. If this article has created concern and/or these terms are brand new to you, pick up the phone and schedule an experience modification control meeting with an advisor from Rancho Mesa at (619) 937-0164. Their Best Practices approach to managing risk starts with a client-centric process that is focused on education and execution.

2019 Expected Loss Rates Published in California’s Updated Regulatory Filing – X-MOD Impact Inevitable for 0042 Class Code

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

The 2019 Expected Loss Rate (ELR) for Landscaping class code 0042 was recently published at a 15% decrease or $2.97.

The ELR is the factor used to anticipate a class code’s claim cost per $100 for the experience rating period. It is not to be confused with the Pure Premium Rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development.

Author, Drew Garcia, Vice President, Landscape Group, Rancho Mesa Insurance Services, Inc.

The 2019 Expected Loss Rate (ELR) for Landscaping class code 0042 was recently published at a 15% decrease or $2.97.

The ELR is the factor used to anticipate a class code’s claim cost per $100 for the experience rating period. It is not to be confused with the Pure Premium Rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development. The PPR includes all of the mentioned above factors and is the rate for which a carrier can expect to pay for all of the cost associated with claims in a specific industry. The PPR does not account for the carrier’s overhead, profit, tax, and commissions.

Under most circumstances, when you hear the word decrease as associated with insurance its a good thing, but in the case of the ELR, a decrease will have a negative impact on your Experience MOD (X-MOD). In simple terms, if your losses stay the same and the ELR for your industry is down 15%, your X-MOD is going to go up.

At 15%, the landscape class code accounts for one of the largest swings in the 2019 regulatory filing for all industries. This only reinforces the importance of mitigating claim frequency, superior carrier claims handling, internal claims advocacy, claim cost consolidation efforts, and a proven system to keep all of these aspects running constantly. Fortunately, Rancho Mesa has a system in place today and it is a proven success.

Don’t be caught off guard in 2019; have a plan and always anticipate for the future. Let Rancho Mesa help manage your landscape insurance needs. For more information, call (619) 937-0164.

Changes in the 2019 Experience Modification Formula – Are You Ready? (Part 2)

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR).

Part 1 of this article describes the Primary Threshold and Expected Loss Rate. Read Part 1 of this article. Part 2 provides an overview of the changes to the EMR calculation.

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR).

Part 1 of this article describes the Primary Threshold and Expected Loss Rate. Read Part 1 of this article. Part 2 provides an overview of the changes to the EMR calculation.

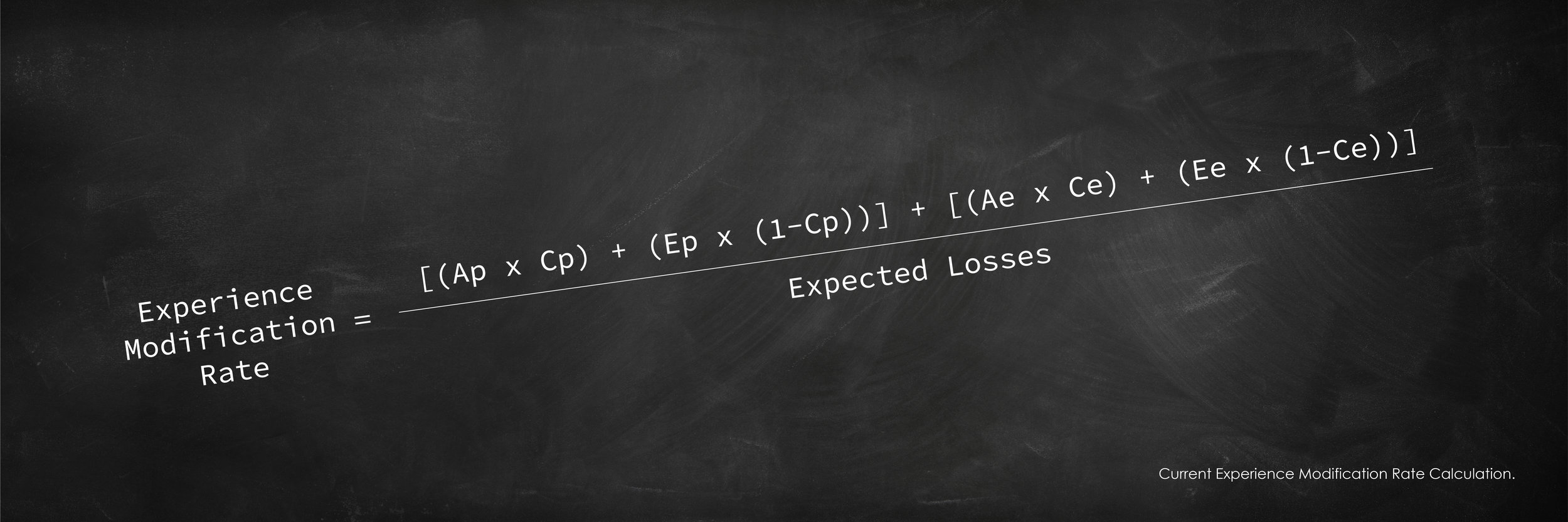

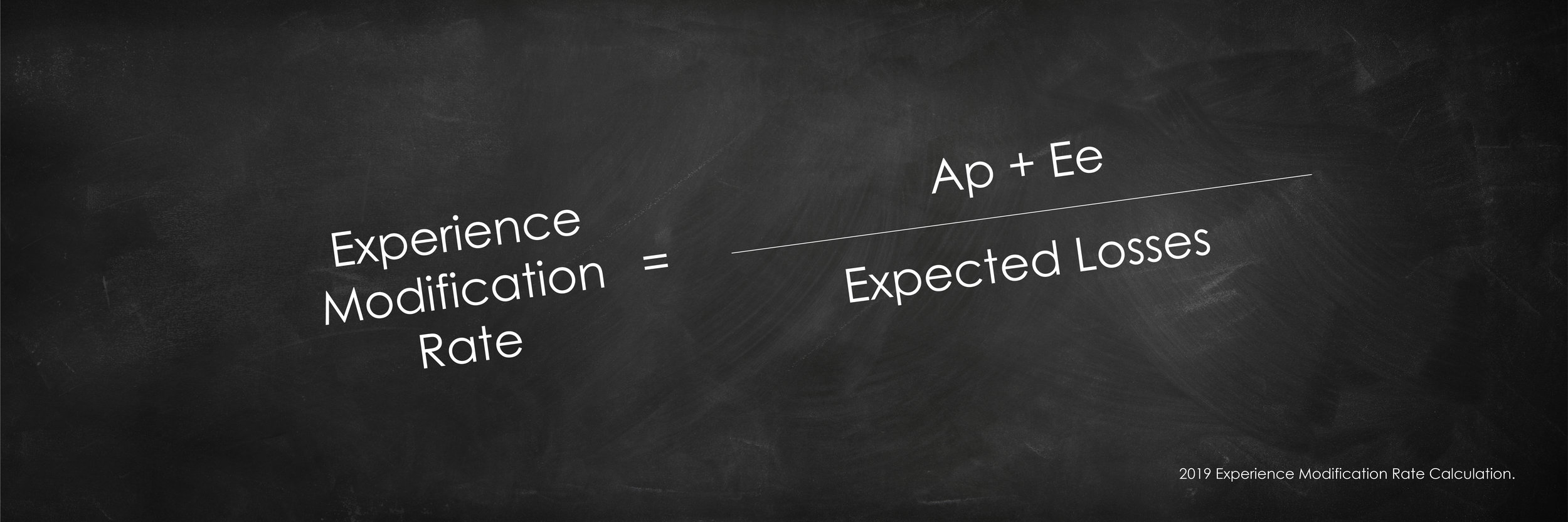

The Simplified Formula

Individual claim cost (i.e., both paid and reserved) will go into the calculation up to the primary threshold limit are considered the actual primary losses. Any claim cost that exceeds your primary threshold is considered the actual excess loss. In past experience mod formulas, the actual excess loss was used in the factoring of your EMR; in 2019, it will have no effect. However, under the new calculation, the industry expected excess losses will be considered in the 2019 simplified formula.

Actual Primary Losses + Expected Excess Losses / Expected Losses

The expected excess losses are calculated by multiplying your class code’s payroll per $100 by the expected loss rate for that same class code. This number is then discounted by the “D Ratio” to determine expected primary losses and expected excess losses. There are 90 different D-Ratios for each classification based on the primary threshold. The D-Ratio is different for each classification and is determined by the severity of injuries that occur within that particular class code.

The first $250 of all claims will no longer be used in the calculation of your EMR.

This is a major change and one that was initiated in part to encourage all employers to report all claims, including those deemed first aid, without having a negative impact on the companys’ EMR. This change will affect all claims within the 2019 calculation; so yes, it will include years previously completed and reported. This will have a positive impact on EMRs in that claim dollars will be removed from the EMR calculation.

Confused – Want more details?

Help is on the way. We are going to hold a statewide webinar on Thursday, October 4th at 9:00am in order to dig deeper into this subject and answer specific questions. You may register for the webinar by contacting Alyssa Burley at (619) 438-6869 or aburley@ranchomesa.com.

Changes in the 2019 Experience Modification Formula – Are You Ready? (Part 1)

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR). Sadly, most businesses are both unaware and unprepared.

Author, David J. Garcia, A.A.I, CRIS, President, Rancho Mesa Insurance Services, Inc.

As we approach 2019, there will be several changes in the experience modification formula that directly affects the calculation of an employer's 2019 Experience Modification Rate (EMR). Sadly, most businesses are both unaware and unprepared.

Before we breakdown the changes to the 2019 EMR formula, we must first have a strong understanding of the two critical components that directly affect the outcome of the EMR. This article will be broken out into 2 parts. Part 1 will describe the Primary Threshold and Expected Loss Rate. In Part 2, I will provide an overview of the changes to the EMR calculation.

The single most important number to my EMR is not my final rating?

Primary Threshold

Rancho Mesa has long taken a stance on the importance of a business owner knowing their primary threshold as it relates to the EMR. Proactive business owners should monitor their primary threshold annually as it is subject to change due to payroll fluctuations, operations, and the annual regulatory filing of the expected loss rate. In general terms, the more payroll associated with your governing class (the class code with the preponderance of your payroll) the higher your primary threshold will be. The primary threshold is unique to every business. The 2019 EMR formula is heavily weighted by the company's actual primary losses, the claim cost (both paid and reserved) that goes into the calculation up the primary threshold amount. Controlling claim cost and knowing your company's primary threshold is the first step to understanding the EMR.

Expected Loss Rates

The expected loss rate is the factor used to anticipate a class code's claim cost per $100 for the experience rating period. The expected loss rate (ELR) is not to be confused with the pure premium rate (PPR). The ELR differs from the PPR in that the ELR simply measures the basic claim cost for a class code without including loss adjustment expense, excess loss load (capped at $175,000 for X-MOD purposes), and loss development. The PPR includes all of the mentioned above factors and is the rate for which a carrier can expect to pay all of the cost associated with claims in a specific industry. The PPR does not account for the carrier’s overhead, profit, tax, and commissions.

The ELR changes, annually. It’s important to monitor the change; if your expected loss rates go down (from our analysis this is the direction most are going) and if nothing else changes, your EMR will go up. Why is this? Again, without going too deep, in simple terms, your EMR is a ratio of actual losses to expected losses. If your expected losses go down, but your actual losses remain the same, then your EMR will go up.

To illustrate this, consider the following. Actual losses are $25,000 and your expected losses are $25,000 your EMR would be 100. Now, if your actual losses stay the same at $25,000, but your expected losses drop to $20,000, your EMR would now be 125%. (There are other factors that would go into the actual calculation, so your actual EMR would be different – this was just to illustrate the expected losses impact to the EMR.)

In Part 2 of this article, will cover the actual changes to the EMR calculation.

For more information about the EMR, contact Rancho Mesa Insurance Services at (619) 937-0164.

Six Reasons a Company’s Experience Modification Could be Recalculated

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately California still maintains some of the highest rates in the country, often times two to three times the nations average.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Workers’ Compensation costs continue to be one of the most costly expenses for business owners in California. With recent reform, California has maintained steady rate decreases in the workers’ compensation marketplace. Unfortunately, California still maintains some of the highest rates in the country, often times two to three times the nations average.

Controlling insurance costs is vital to staying profitable and often times, staying in business. An important way business owners can control their insurance costs is by controlling their Experience Modification or X-MOD. An X-MOD is a benchmark of an individual employer against others in its industry, based on that employer's historical claim experience. This comparison is expressed as a percentage which is applied to an employer's workers' compensation premium.

The premium impact of a credit X-MOD (less than 1) vs a debit X-MOD (more than 1) can be significant. Business owners budget around their insurance costs. When there are unforeseen changes to their insurance costs it can have a dramatic effect. While it is rare, there are situations when an X-MOD can change in the middle of a policy term. Below are six circumstances when this could happen:

- If a claim that has been used in an X-MOD calculation is subsequently reported as closed mid policy term AND closed for less than 60% of the aggregate of the highest value, then the X-MOD is eligible for recalculation.

- In cases where loss values are included or excluded through mistake other than error of judgement. Basically, this rule takes into consideration the element of human error.

- Where a claim is determined non-compensable. Meaning the injury was determined to be non-work related.

- Where the insurance company has received a subrogation recovery or a portion of the claim cost is declared fraudulent.

- Where a closed death claim has been compromised over the sole issue of applicability of the workers’ compensation laws of California. Basically, if a person passes away at work but it was determined that the person had a pre-existing condition which caused the death, not work itself.

- Where a claim has been determined to be a joint coverage claim. This occurs mainly with cumulative trauma claims where there was no specific incident that caused an injury, but an injury that developed over time (i.e., wear and tear).

If any of the circumstances above have occurred, than a revised reporting shall be filed with the Workers’ Compensation Insurance Rating Bureau (WCIRB) and it shall be used to adjust the current and two immediately preceding experience ratings.

If you would like to discuss this topic in further detail, and learn how Rancho Mesa Insurance can audit your X-MOD worksheet for potential recalculations, please contact us at (619) 937-0164.

Ask the Expert: Insurance Questions from the Lawn and Landscape Industry

Author, Drew Garcia, NALP National Program Director, Rancho Mesa Insurance Services, Inc.

Drew Garcia answers common insurance questions for the landscape industry.

Author, Drew Garcia, NALP National Program Director, Rancho Mesa Insurance Services, Inc.

How can I control and/or lower my experience rating?

Without getting into detail about the formula or governing insurance bodies, here are some key items to focus on in order to lower your experience rating (i.e., experience modification, MOD), no matter your jurisdiction.

Frequency vs. Severity (Proactively Track and Eliminate the Claim Before it Happens)

Analyze your work related injuries and near misses to search for trends that will help to prevent similar claims from occurring. Your rating will typically see more of a negative impact with multiple claims (frequency) as opposed to one large loss (severity). Frequency drives the probability for more claims to occur in the future which would make your company a higher risk to insurer.

Return to Work (Make it Mandatory)

All claims may potentially impact the experience rating in one way or another, with frequency having a large role in the mathematical formula. Another key part of managing claim costs is the focus on reducing indemnity expenses on every claim. By returning an employee to work you eliminate any claim cost that would have been allocated to temporary disability. The savings you will see on your experience MOD is remarkable. If you need help creating a return to work program, reach out to your workers compensation insurance carrier for guidance. If you decide to implement any of these strategies going forward, implement a mandatory Return to Work program.

Example:

An injured employee will earn $400 a week on temporary disability and is estimated to need three months of recovery. The claim closes three months later with a total incurred claim cost of $4,800 in indemnity (wages) and $2,000 in medical, equaling $6,800.

With a Return to Work program, the injured employee is right back to work on modified duty and earns no temporary disability. The claim closes for $2,000. Not only will the claim have less of an effect on your experience MOD, but you will also have constant communication with the injured employee, which keeps them feeling part of the team, boosts their morale, and perhaps expedites the length of the injury.

Carrier Analytics (Save a $1 Today That Will Cost You $5 in the Future)

Who is handling your insurance claims? When you purchase workers compensation insurance, you are buying a company’s ability to handle claims and how those claims are handled will determine your experience MOD, your cost, and your bottom line for years to come. Carrier benchmarking reports are becoming critical in helping to evaluate the impact each carrier will have on your claim experience. You should place your insurance with a carrier who has a history of writing policies for your specific industry and a proven track record of closing claims faster than the industry, and for less money, because that money is what drives your modifier through the roof.

What are your thoughts on a safety incentive program?

I would suggest safety recognition as opposed to safety incentive, here’s why. An incentive program might keep employees from reporting work related injuries in fear that they might “ruin” a streak of consecutive days without an injury. You do not want to make an employee fearful of reporting an injury. OSHA and the Department of Labor have started to enforce these “dis-incentive” programs in a more visible way.

Safety recognition would mean identifying an employee who has successfully executed your company’s standard safety requirements or has gone above and beyond to better the company’s safety culture. A type of recognition could be handing out raffle tickets to employees who have executed standard safety protocol and having a monthly drawing for prizes.

What is the key to having a safe company? We have all the safety programs; we do tailgates every week; and, we still have claims, routinely!

In one word, the companies that experience the best safety records all share this common trait, communication. You can have all the compliance based safety programs in place but without superior communication they will lack true execution. Proactively communicating with your team in the field, every day, is what it takes. Safety must become a common attribute employees think of when they talk about your company. It takes participation and “buy-in” on all levels from ownership to employee. Employees must understand the exposures and job hazards associated with their work, but, the culture you are trying to create within your company should generate excellent decision making, like employees who think:

- “I probably shouldn’t lift this alone.”

- “That slope looks wet."

- “I should pick this up before someone steps on it.”

You cannot buy a good safety company. Like anything in life, it is earned. With a concentrated effort, you can establish a solid safety program that becomes routine and everyone in your company will benefit from it.

Experience Modification Factors and the Pre-Qualification Process

Author Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

As we enter 2018, government agencies, project owners and general contractors often require subcontractors to enter their pre-qualification process. Many of these entities will look closely at your Experience Modification Rate (EMR).

Author Sam Clayton, Vice President, Construction Group, Rancho Mesa Insurance Services, Inc.

As we enter 2018, government agencies, project owners and general contractors often require subcontractors to enter their pre-qualification process. Many of these entities will look closely at your Experience Modification Rate (EMR).

EMR is a numeric representation of a company’s payroll and claims history, compared to businesses in the same industry or standard industry classification. EMRs create a common baseline for businesses while allowing for a surcharge when employers' claims are worse than expected and credit when employers' claims are better than the industry average. More specifically, companies with an EMR rate of 1.00 are considered to have an average loss experience. Factors greater than 1.00 are considered worse than average, while less than 1.00 are considered better than average.

Pre-Qualification Process

In the highly competitive world of construction bidding, it has become more common that contractors can be precluded from the pre-qualification process due solely to above average EMRs. This represents an oversight as many companies have strong, well-developed safety programs, yet their EMR is holding them back. Some examples of this are:

- EMRs are lagging factors. They only factor the last three policy periods, not including the current policy period.

- EMRs can include claims that may have been unavoidable and do not represent a lack of safety (i.e. an employee is rear ended by an uninsured motorist).

- Large severity claims from smaller sized companies can impact the EMR much more negatively than a similar sized claims at a larger firm.

- The effectiveness of claims handling may vary from one insurance company to another, thus impacting certain employers when cases remain open with high reserves.

Rather than placing such a critical importance on the EMR Rate, owners and contractors designing the pre-qualification document should include frequency indicators like incident and DART Rate (i.e., days away, restricted or transferred) forms. These measuring tools incorporate current year totals and can provide up to 5 years of historical data. Incident Rate calculations indicate how many employees per 100 have been injured under OSHA rules within the specific time period. The DART rate looks at the amount of time an injured employee is away from his or her regular job. Lastly, contractors attempting to become pre-qualified should have the ability to provide a detailed explanation should their EMR exceed 100. This can include loss data, a summary of the company’s Illness and Injury Prevention Plan (IIPP) and code of safe practices, and more information on what exactly the company is doing to reduce future exposure to loss.

Given the importance of the pre-qualification process and the potential for contractors to be precluded from new opportunities to bid work, we’ve developed a “Best Practices” approach to assist companies in managing their EMR.

Managing Your EMR with Best Practices

The Best Practices approach to high EMRs includes a total claim physical, claims advocacy, and implementation of the Risk Management Center.

Total Claim Physical

The total claim physical accurately identifies your company's strengths and weaknesses, and then scores the company against others in the industry. It includes an audit of the EMR, analysis of claim frequency and severity, claim trends and determine root causes, provide quarterly claims reviews, and conduct pre-unit stat meetings.

Claims Advocacy

Utilizing a claims advocate can decrease existing claim costs, reduce excessive reserves, and expedite claim closures, which can reduce the EMR.

Risk Management Center

The Risk Management Center provides access to safety training materials and tracking, analysis of incidents and OSHA reporting, monthly risk management workshops and webinars.

For more information on managing your EMR before the pre-qualification process, contact Rancho Mesa Insurance Services at (619) 937-0164.