Industry News

Employers Enlist Assistance from HR Experts while Navigating Perils of COVID-19

Author, Chase Hixson, Account Executive, Rancho Mesa Insurance Services, Inc.

The COVID-19 pandemic has brought a slew of unknowns to employers across the country, especially as it relates to human resources questions and Employment Practices Liability (EPLI). Rancho Mesa’s RM365 HRAdvantage™ Portal has been a favorite of our clients ever since its release in 2019. The portal continues to grow in popularity as employers face new challenges as workplace standards and employee interaction changes, almost daily.

The COVID-19 pandemic has brought a slew of unknowns to employers across the country, especially as it relates to human resources questions and Employment Practices Liability (EPLI). Rancho Mesa’s RM365 HRAdvantage™ Portal has been a favorite of our clients ever since its release in 2019. The portal continues to grow in popularity as employers face new challenges as workplace standards and employee interaction changes, almost daily.

The most popular tool in the portal gives clients access to live certified Senior Professionals in Human Resources (SPHR) and Professionals in Human Resources (PHR) advisors via phone or through the portal’s messaging tool. Not only will the HR experts answer human resources questions, they will also follow-up with written documentation of the advice so you can refer back to their recommendations.

If an effort to ensure compliance and reduce the chance of an EPLI claim, Rancho Mesa clients are reaching out to our experts for advice on how to navigate human resource issues before they turn into a legal nightmare.

A recent client inquiry included a question about: “required postings and notifications regarding COVID-19 and how to deliver them to remote employees.” The HR experts provided guidance on how to address the client’s specific situation like getting state notices to employees who are working from home.

Another client asked “what to do if an employee refuses to come to work when restrictions are lifted.” The advice pointed to the federal Families First Coronavirus Response Act (FFCRA) and possible city ordinances or state law that may dictate how to handle the specific situation. In addition, other factors were highlighted that take into account the employee’s personal risk factors and the Occupational Safety and Health Administration (OSHA) rules for safe workplaces.

Additionally, our team is answering questions like “Can employers require employees to get tested for COVID?” or “What accommodations am I required to make for employees working from home?”

Getting reliable answers to important human resources questions quickly can mean the difference between a happy and healthy workforce, and a possible EPLI claim.

With so much uncertainty facing our clients, many have found comfort and confidence in knowing they have reliable human resources experts available to advise them as they navigate these uncharted waters.

If you have any further questions about EPLI coverage, please contact Rancho Mesa Insurance Services at (619) 937-0164.

How Will Job Losses and the New Normal Workplace Triggered by COVID-19 Impact Employment Practices Liability?

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

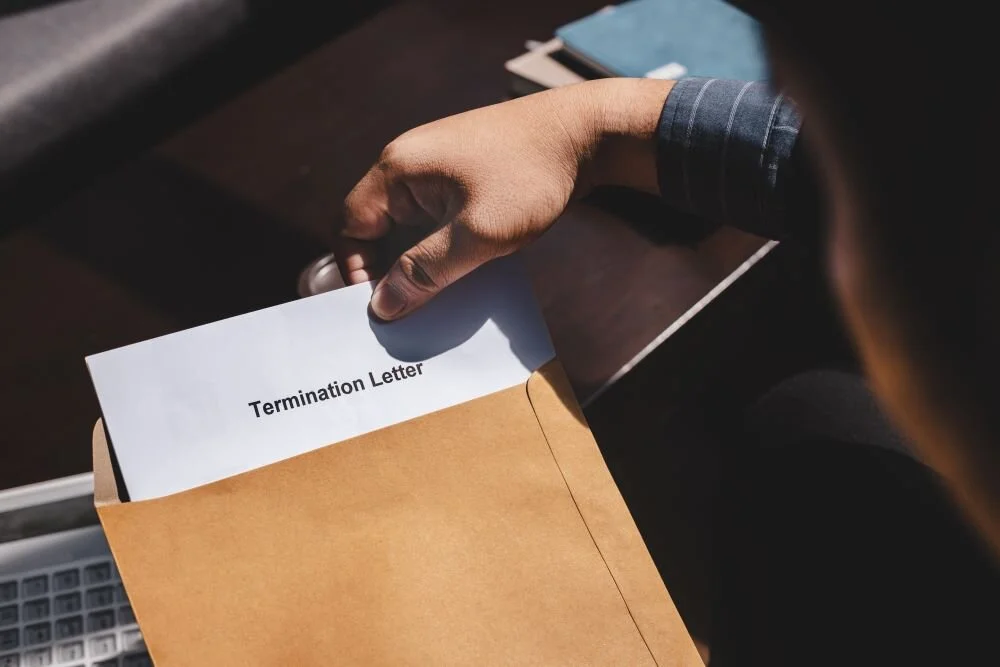

As insurance companies brace for a spike in claim filings due to COVID-19, one under the radar coverage that could be severely impacted is Employment Practices Liability (EPLI). With just over 22,000,000 employees recently laid off, terminated or furloughed nationwide, most experts anticipate that EPLI claim frequency will jump.

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

As insurance companies brace for a spike in claim filings due to COVID-19, one under the radar coverage that could be severely impacted is Employment Practices Liability (EPLI). With just over 22,000,000 employees recently laid off, terminated or furloughed nationwide, most experts anticipate that EPLI claim frequency will jump.

As an example, if just 1% of those employees referenced above filed wrongful termination claims, the EPLI industry could potentially see 220,000 new cases. This possibility alone, and the continued uncertainty with the economy, will very likely change how underwriters approach current pricing, retentions, exclusions, and other coverage terms.

The often mentioned “new normal” workplace requires us to proceed with caution to ensure your organization is protected against potential EPLI claims. Coupled with the exposure to wrongful termination suits, additional claim scenarios are unfolding daily that can include the following:

Certain groups of employees are targeted because of their national origin or because of suspicion of being infected, causing a discrimination or harassment claim.

Invasion of privacy concerns if employees are questioned about personal travel, health history, or family health history.

Employees may opt out of work-related events or meetings and believe they were retaliated against which could trigger a claim.

As an employer, having access to resources and responsive feedback from real people in this highly sensitive time remains critical. Rancho Mesa’s RM365 HRAdvantage™ platform provides our clients with a team of compliance experts that can walk you through these and many other COVID-19 related employer challenges. Visit Rancho Mesa’s Risk Management and Human Resource page to take the next steps.

Optimizing Risk Management While Reducing Gaps in Coverage

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Working within the construction unit at Rancho Mesa for over 15 years, I have developed strong long-term business relationships with my clients. As an insurance advisor, I have an obligation to insulate clients from exposures and liabilities. Many of which may remain the same from year to year. However, it is vital that business owners meet with their insurance advisor frequently, especially prior to an insurance renewal, to avoid potential gaps in coverage. Below are a few key topics that should be reviewed on a regular basis by a company’s insurance advisor.

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

Working within the construction unit at Rancho Mesa for over 15 years, I have developed strong long-term business relationships with my clients. As an insurance advisor, I have an obligation to insulate clients from exposures and liabilities. Many of which may remain the same from year to year. However, it is vital that business owners meet with their insurance advisor frequently, especially prior to an insurance renewal, to avoid potential gaps in coverage. Below are a few key topics that should be reviewed on a regular basis by a company’s insurance advisor.

Review and Discuss Business Operations

It’s always a good business practice to have the insurance advisor review the business’s operations to see if there have been any changes that could affect its risk profile. For example, I once had a client in the construction industry that specialized in commercial tenant improvement work. The company wanted to start a residential construction division. By understanding this change before it actually took place it provided us the time to adequately access the differences in the insurance exposures between the commercial and residential marketplace. As a result, we were able to proactively and affordably place their coverage with an insurance carrier that was comfortable with both exposures.

Review Financial Projections

With the economy fluctuating year to year, it is vital that you meet with your insurance advisor and go over your financial projections for the coming policy term. These items should include projected; annual sales, payrolls, subcontract costs and any changes in your surety requirements. These factors will help in not only negotiating the most favorable renewal terms for you but help to avoid any unforeseen expenses like a large final audit

Discuss Business Assets

Businesses routinely buy, sell, and upgrade their tools, equipment, and vehicles. While most are conditioned to notify their insurance advisor of any changes, it is always a good business practice to review assets with the insurance advisor at each pre-renewal meeting. It is common that there are items that were either sold (that need to be removed) or new (that need to be added to policies). By reviewing the assets on a regular basis, it minimizes the chance that items are missed and you either are paying premium on an item you no longer have or have an uninsured loss.

Discuss and Revisit Recommended Coverages

Recommended coverages may include an Umbrella, Pollution Liability, Professional Liability, Employment Practices Liability, and Cyber Liability policies. Even if you have discussed these coverages in the past with your insurance advisor and have declined them, they should not assume you will do so again in the future. The business climate is constantly changing; therefore, so are the risks you are facing. Understanding where you have gaps in your risk management profile and making informed decisions to either transfer the risk to an insurance carrier (purchase insurance) or retain the risk yourself (don’t purchase insurance) is always a Best Practices standard.

If you would like to discuss and learn more about Rancho Mesa’s proprietary risk management tools and explore our help in developing a Risk Management program based on your specific business needs, you can reach out to me at 619-937-0174.