Industry News

The Crucial Role of Third-Party EPLI Coverage for Tree Care Companies

Author, Rory Anderson, Partner, Account Executive, Rancho Mesa Insurance Services, Inc.

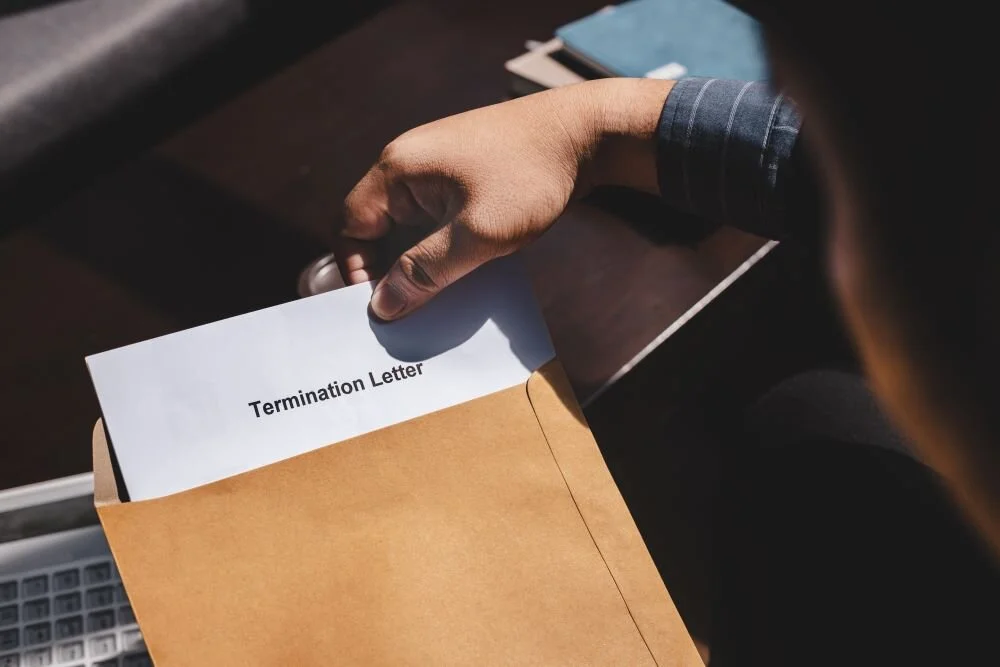

Operating a tree care business comes with numerous risks, from ensuring your team’s safety on the job to managing potential property damage. One crucial area of risk that is often overlooked is Employment Practices Liability Insurance (EPLI), specifically third-party coverage. Third-party EPLI can help protect your business from expensive lawsuits, making it essential for businesses that regularly interact with the public.

Author, Rory Anderson, Partner, Account Executive, Rancho Mesa Insurance Services, Inc.

Operating a tree care business comes with numerous risks, from ensuring your team’s safety on the job to managing potential property damage. One crucial area of risk that is often overlooked is Employment Practices Liability Insurance (EPLI), specifically third-party coverage. Third-party EPLI can help protect your business from expensive lawsuits, making it essential for businesses that regularly interact with the public.

EPLI Coverage

EPLI is an insurance policy designed to protect businesses from claims related to employment practices. This includes allegations of discrimination, harassment, wrongful termination, and other workplace-related issues brought forth by employees. For many companies, EPLI is vital for covering the costs of defending against lawsuits, including legal fees, settlements, and damages.

While traditional EPLI coverage protects your business against employee claims, it is important to also consider third-party EPLI coverage.

Third-Party EPLI Coverage

Third-party EPLI coverage extends the protection of your EPLI policy beyond your employees. This provides an extra layer of protection for claims made by non-employees, such as customers, vendors, and members of the public. It covers allegations made by non-employees who may claim they were subject to harassment, discrimination, or wrongful conduct by your employees while interacting with your business. In the tree care industry, where workers frequently engage with clients, contractors, and the general public, this type of coverage is important.

Examples of Third-Party EPLI Claims in Tree Care

Harassment Allegation from a Homeowner. A tree care crew is performing work on a residential property when a homeowner accuses one of the employees of making inappropriate comments or gestures. The homeowner files a lawsuit for emotional distress, potentially resulting in costly legal fees.

Inappropriate Behavior from an Arborist in a Bucket Truck. While performing tree pruning, an arborist in a bucket truck sees a woman through a window who appears to be changing clothes. The woman later claims the arborist was staring at her inappropriately and files a harassment lawsuit against the tree care company. Even if the arborist did not intend any harm, this type of situation can lead to legal action and unnecessary costs.

Reasons Third-Party EPLI Coverage Is Essential for Tree Care Companies

High Interaction with the Public. Arborists and tree care crews often work in public spaces or on residential and commercial properties where they have frequent contact with non-employees, increasing the likelihood of third-party claims.

Legal Defense Costs. The costs of legal defense can add up quickly, whether or not your business is found liable. Third-party EPLI coverage can help offset these costs, preventing them from becoming a financial burden on your company.

EPLI Policy

Third-Party Coverage. Not all EPLI policies automatically cover claims made by non-employees. Be sure to confirm that third-party protection is included.

Defense Cost Outside Limit. If defense costs are deducted from the liability limit, they can quickly deplete your coverage, leaving less available for a settlement or judgment. It is crucial to look for a policy that offers defense costs outside the limit, ensuring that your liability coverage remains intact and fully available in the event of a claim.

Third-party EPLI coverage is an essential safeguard for tree care businesses, providing protection against claims made by non-employees such as homeowners, pedestrians, or subcontractors. With the high level of public interaction in this industry, the potential for costly lawsuits is significant. Ensuring your EPLI policy includes third-party coverage and defense costs outside the liability limit can help protect your business from unexpected legal and financial burdens.

To learn more about how EPLI insurance can protect your company, contact me at (619) 486-6437 or randerson@ranchomesa.com.

A Hardening Employment Practices Marketplace Likely to Impact Many Businesses

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

The Employment Practices Liability Insurance (EPLI) marketplace has faced a number of factors that are contributing to skyrocketing premiums and deductibles. Many insurance companies are facing the choice of whether to remain in the marketplace or exit altogether. Those willing to remain are then faced with having to consider the following changes…

Author, Jeremy Hoolihan, Account Executive, Rancho Mesa Insurance Services, Inc.

The Employment Practices Liability Insurance (EPLI) marketplace has faced a number of factors that are contributing to skyrocketing premiums and deductibles. Many insurance companies are facing the choice of whether to remain in the marketplace or exit altogether. Those willing to remain are then faced with having to consider the following changes:

Increase their premiums to offset increased claim activity

Increase their deductibles

Consider adding exclusions of previously covered exposures

Consider only renewing existing clients’ policies

Pulling out of certain business segments such as retail, hospitality, leisure, and transportation which is currently being impacted the most from COVID-19.

Below are some of the main factors causing the hardening EPLI marketplace. As you will see, they vary significantly but combined they have created a perfect storm.

COVID-19

These are unprecedented times with businesses being forced to shut down for months due to COVID-19, employees having to work remotely and our economy seemingly coming to a standstill. Couple this with a significant increase in layoffs, severance packages, furloughs, and unemployment, and we have seen a significant increase in claims filed. By January 2021, the plaintiff’s bar had filed over 1,200 COVID-19 related employment lawsuits. These types of lawsuits have continued to grow each month since the pandemic began.

We have also seen the unemployment rate spike from 3.5% in March of 2020 to 14.7% in April 2020. Currently the unemployment rate has settled to about 8% but this still represents a double digit increase from2019.

EPLI claims often follow large changes in workforce, including reductions, promotions and demotions. Three areas of particular growing concern include:

Sexual Harassment

Privacy

Retaliation

Sexual Harassment

The heightened awareness and increased public intolerance for harassment developed in part from the #MeToo movement has given a voice to people that are now not only speaking out but filing lawsuits against their employer for sexual harassment. This national attention has also altered the legal environment surrounding these types of claims, often leading to much higher settlements outcomes.. Industry wide, the total monetary benefits awarded to sexual harassment victims has increased 68% from 2016 to 2019 according to the U.S. Equal Employment Opportunity Commission.

Privacy

In addition to discrimination and sexual harassment claims, insurance carriers also anticipate privacy-related claims. As businesses begin to reopen, there are new policies and procedures in place that require a Human Resources department to question employees about their personal health, their health history, and their family’s health history. The nationwide Health Insurance Portability and Accountability Act (HIPAA) and other state-specific laws like the Illinois Biometric Information Privacy Act (BIPA) regulates how companies collect, store, use, and share biometric information. With temperature-taking requirements and a certification form filled out, there is a concern that some employees may feel their privacy has been invaded.

Retaliation

There is also a growing concern that there will be more retaliation type claims relating to an employee’s use of social media. With COVID-19 in mind, employees are already expressing their concerns via social media about their employers’ lack of safety measures or personal protective equipment (PPE). It’s reasonable to consider that if these employees are terminated that they may feel they were retaliated against because of their posts.

Retaliation could also be a result of employees exercising their rights under Family Medical Leave Act (FMLA) or other benefits such as workers compensation or paid sick leave.

US Supreme Court LGBTQ Decision

The Supreme Court ruled in June 2020 that Title VII of the 1964 Civil Rights Act protects employees from discrimination based on sexual orientation and gender identification.

Previously only 28 States awarded such protections. Now that these protections are law in all 50 states, we will likely see additional claims alleging employment discrimination based on gender identity and sexual orientation.

In conclusion, running a business remains a challenge under normal circumstances. Add in the many side effects of the pandemic and it can feel overwhelming. EPLI-related claims can result in catastrophic financial impacts to a company’s balance sheet. The cost of defending your business alone can potentially put a company out of business. While EPLI premiums continue to rise, so does your exposure to a myriad of claims that fall under this coverage umbrella. Having EPLI in place can mean the difference between absorbing fair and reasonable claim costs or forcing an uninsured business to close their doors. To learn more about EPLI coverage and ways to construct a policy that meets your needs, please reach out to me at 619-937-0174 or jhoolihan@ranchomesa.com.

2021 Insurance Game Plan

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

As we come to the end of 2020, the most challenging year most of us have ever experienced, where COVID-19, wild fires and other natural disasters took their toll emotionally, physically, mentally and financially on all of us we can only hope for a brighter 2021.

Author, Dave Garcia, President, Rancho Mesa Insurance Services, Inc.

As we come to the end of 2020, the most challenging year most of us have ever experienced, where COVID-19, wild fires and other natural disasters took their toll emotionally, physically, mentally and financially on all of us, we can only hope for a brighter 2021.

The insurance industry did not escape the impact of COVID-19 and the natural disasters, either. Insurance companies, along with their reinsurance companies, suffered catastrophic losses as a result. As with many industries, there will be lagging actions that will take place in 2021 to help these companies in their efforts to recover.

While there really isn’t a line of insurance that wasn’t impacted, the lines of insurance that suffered the greatest losses and impacts include:

Property

General Liability

Excess/Umbrella

Workers’ Compensation

EPLI

Cyber Liability

Surety

Employee Benefits

For this article, I will limit my discussion to the property and casualty lines and leave surety and employee benefits to another day.

To offset these losses, I anticipate any number of steps insurance companies will take as we move into 2021. But, let me just touch on those that I think will have the greatest impact and need for attention to business owners in 2021.

Let’s review these and I will try and give you a small sampling of the implications for each action.

Non-renewing policies

Carriers in many cases will not offer renewal terms.

Reducing coverage limits and terms

Increasing deductibles, lowering aggregate limits particularly in the excess/umbrella marketplace.

Add new exclusions

Businesses will start to see “communicable disease” exclusions added to various lines of insurance.

Increase underwriting information needed

A higher emphasis on information particularly as it relates to a business’s policies and procedures to mitigate COVID-19.

Raise premiums

This is the ultimate consequence and one we are all anticipating to see beginning in early 2021.

To many businesses, this will seem daunting and hopeless - one more hurdle to overcome to keep their businesses going. However, there are proactive steps you can take to mitigate these circumstances and have a strong year despite the adversity.

I’m a firm believer in being pro-active and not re-active. Following are steps you can take to meet this challenge head on:

Meet with your insurance advisor 90-120 days from your renewal date.

Understand the specific challenges you will be facing.

Create a strategy on how to approach the insurance marketplace to ensure the most cost effective and comprehensive risk management program.

Review and enhance your existing safety program. Rancho Mesa offers our RM365 Advantage Safety Star™ certification program. This is a comprehensive web-enabled training course designed to enable your employees from supervisory to front-line workers to be trained and certified in safety best practices. The insurance marketplace already places a high value on these types of safety trainings and certifications, so this will help your company’s productivity through fewer claims but also position you in a more favorable position in the marketplace.

Benchmark your company’s safety performance to your industry and see which areas you are outperforming your peers and areas that need your attention. Rancho Mesa offers a benchmarking report we call StatTrac™ to our clients or to other companies who want to see where they stack up.

To close, let me reassure you there is light at the end of the tunnel for 2021. Be proactive; start 90-120 day out from your renewal; don’t let insurance issues sneak up on you; attack them head on and I believe you can make 2021 a great year for you and your company.

If you have any questions or want any help in devising a plan and you are a construction company, please reach out to Sam Clayton, our Construction Group Leader at sclayton@ranchomesa.com. If you are in the human services industry, schools, non-profit, healthcare, assisted living, etc., please reach out to Sam Brown, our Human Services Group Leader. And finally, we can be reached at (619) 937-0164 or at our website, www.ranchomesa.com.

I really believe there is no limit to what you can do – best of luck in 2021.

Employers Enlist Assistance from HR Experts while Navigating Perils of COVID-19

Author, Chase Hixson, Account Executive, Rancho Mesa Insurance Services, Inc.

The COVID-19 pandemic has brought a slew of unknowns to employers across the country, especially as it relates to human resources questions and Employment Practices Liability (EPLI). Rancho Mesa’s RM365 HRAdvantage™ Portal has been a favorite of our clients ever since its release in 2019. The portal continues to grow in popularity as employers face new challenges as workplace standards and employee interaction changes, almost daily.

The COVID-19 pandemic has brought a slew of unknowns to employers across the country, especially as it relates to human resources questions and Employment Practices Liability (EPLI). Rancho Mesa’s RM365 HRAdvantage™ Portal has been a favorite of our clients ever since its release in 2019. The portal continues to grow in popularity as employers face new challenges as workplace standards and employee interaction changes, almost daily.

The most popular tool in the portal gives clients access to live certified Senior Professionals in Human Resources (SPHR) and Professionals in Human Resources (PHR) advisors via phone or through the portal’s messaging tool. Not only will the HR experts answer human resources questions, they will also follow-up with written documentation of the advice so you can refer back to their recommendations.

If an effort to ensure compliance and reduce the chance of an EPLI claim, Rancho Mesa clients are reaching out to our experts for advice on how to navigate human resource issues before they turn into a legal nightmare.

A recent client inquiry included a question about: “required postings and notifications regarding COVID-19 and how to deliver them to remote employees.” The HR experts provided guidance on how to address the client’s specific situation like getting state notices to employees who are working from home.

Another client asked “what to do if an employee refuses to come to work when restrictions are lifted.” The advice pointed to the federal Families First Coronavirus Response Act (FFCRA) and possible city ordinances or state law that may dictate how to handle the specific situation. In addition, other factors were highlighted that take into account the employee’s personal risk factors and the Occupational Safety and Health Administration (OSHA) rules for safe workplaces.

Additionally, our team is answering questions like “Can employers require employees to get tested for COVID?” or “What accommodations am I required to make for employees working from home?”

Getting reliable answers to important human resources questions quickly can mean the difference between a happy and healthy workforce, and a possible EPLI claim.

With so much uncertainty facing our clients, many have found comfort and confidence in knowing they have reliable human resources experts available to advise them as they navigate these uncharted waters.

If you have any further questions about EPLI coverage, please contact Rancho Mesa Insurance Services at (619) 937-0164.

How Will Job Losses and the New Normal Workplace Triggered by COVID-19 Impact Employment Practices Liability?

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

As insurance companies brace for a spike in claim filings due to COVID-19, one under the radar coverage that could be severely impacted is Employment Practices Liability (EPLI). With just over 22,000,000 employees recently laid off, terminated or furloughed nationwide, most experts anticipate that EPLI claim frequency will jump.

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

As insurance companies brace for a spike in claim filings due to COVID-19, one under the radar coverage that could be severely impacted is Employment Practices Liability (EPLI). With just over 22,000,000 employees recently laid off, terminated or furloughed nationwide, most experts anticipate that EPLI claim frequency will jump.

As an example, if just 1% of those employees referenced above filed wrongful termination claims, the EPLI industry could potentially see 220,000 new cases. This possibility alone, and the continued uncertainty with the economy, will very likely change how underwriters approach current pricing, retentions, exclusions, and other coverage terms.

The often mentioned “new normal” workplace requires us to proceed with caution to ensure your organization is protected against potential EPLI claims. Coupled with the exposure to wrongful termination suits, additional claim scenarios are unfolding daily that can include the following:

Certain groups of employees are targeted because of their national origin or because of suspicion of being infected, causing a discrimination or harassment claim.

Invasion of privacy concerns if employees are questioned about personal travel, health history, or family health history.

Employees may opt out of work-related events or meetings and believe they were retaliated against which could trigger a claim.

As an employer, having access to resources and responsive feedback from real people in this highly sensitive time remains critical. Rancho Mesa’s RM365 HRAdvantage™ platform provides our clients with a team of compliance experts that can walk you through these and many other COVID-19 related employer challenges. Visit Rancho Mesa’s Risk Management and Human Resource page to take the next steps.

What Do You Mean My Deductible Is Infinity?

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

In this unsettling time throughout various workforces, it makes good business sense to consider EPLI options with varied deductible ranges. Having that clarity brings comfort to many clients who have worked years to build their business, acquire assets, and improve their net worth. Exposing their business to what could very well be unlimited costs creates considerable risk moving forward.

Author, Kevin Howard, CRIS, Account Executive, Rancho Mesa Insurance Services, Inc.

Employment Practices Liability Insurance (EPLI)

Employment Practices Liability Insurance (EPLI) can protect companies from claims related to wrongful termination, discrimination, defamation, unfair hiring/firing practices, and wage and hour lawsuits. EPLI policies may also provide defense costs associated with responding to employment related lawsuits.

HIGHER THAN AVERAGE DEDUCTIBLES

With the increasing frequency of EPLI claims and 40% of California claims occurring within companies with less than 100 employees, deductibles have risen to previously unseen levels. It is now common to see per claim deductibles at a $10,000 starting point and jumping as high as $50,000. These higher retentions can, at times, deter many employers from securing coverage when they might need it most.

YOUR DEDUCTIBLE IS INFINITY

For those employers who elect to self-insure this exposure and go bare without a policy, there is a question that needs to be asked. What is your deductible without EPLI coverage? The simple, very possible answer is that it can be infinity. That is, an employer is responsible for the first dollar to defend along with any future negotiated settlement. That unknown is why many of our clients ultimately purchase EPLI as their balance sheet cannot absorb an infinite loss.

ATTENTION BUSINESS OWNERS!!!

In this unsettling time, across various workforces, it makes good business sense to consider EPLI options with varied deductible ranges. Having that clarity brings comfort to many clients who have worked years to build their business, acquire assets, and improve their net worth. Exposing their business to what could very well be unlimited costs creates considerable risk moving forward.

COMMON MISCONCEPTIONS

Misconception: “If I file an EPLI claim, I will owe the entire deductible upfront.”

Truth: When a claim is filed, policy holders will team up with an attorney who will bill hours until your self-insured retention is met. This could run the course of years with small bills being paid out over time.

Misconception: “I can’t afford to pay an entire annual premium at once, on top of my other insurance renewal premiums.”

Truth: Rancho Mesa can generate a finance plan that will allow you to pay your premiums over a 12 month period.

Misconception: “If I ever have a claim occur, I will just purchase a policy at that time to protect my business.”

Truth: EPLI carriers include prior acts exclusion for this very reason. Any claim that has been made, even in its infant stages, will be declined. You must have a policy in place in advance in order to protect yourself.

Misconception: “I have never had an EPLI claim. Why would I have one now?”

Truth: The California mandate AB 1825 and SB 1343 have increased awareness and visibility of employment related lawsuits. In light of workplace discrimination concerns and the #MeToo movement, the State of California requires all employers with more than 5 employees to conduct Sexual Harassment Prevention Training.

Misconception: “My general liability policy covers EPLI.”

Truth: General liability carriers exclude employment practices liability. If you were to file a claim they would deny coverage.

Business owners deserve a clear explanation of ways to protect themselves from insurable risk. If you would like to discuss how your business is protected, please contact Rancho Mesa Insurance Services, Inc. at (619) 937-0164.

Ensuring CA Sexual Harassment and Abusive Conduct Training is SB 1343 Compliant

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

In September 2018, former California Governor Jerry Brown approved Senate Bill 1343 (SB 1343) which expanded the requirements for Sexual Harassment and Abusive Conduct Prevention training within California workplaces.

In order for the Sexual Harassment and Abusive Conduct Prevention training to be compliant, it must meet the following requirements. The training must:

Editor’s Note: This article was originally published on February 7, 2019 and has been updated for accuracy on September 12, 2019.

Author, Alyssa Burley, Client Services Coordinator, Rancho Mesa Insurance Services, Inc.

In September 2018, former California Governor Jerry Brown approved Senate Bill 1343 (SB 1343) which expanded the requirements for Sexual Harassment and Abusive Conduct Prevention training within California workplaces.

“An employer who employs 5 or more employees, including temporary or seasonal employees, [is required] to provide at least 2 hours of sexual harassment training to all supervisory employees and at least one hour of sexual harassment training to all nonsupervisory employees by January 1, 2020, and once every 2 years thereafter, as specified,” according to SB 1343.

On August 30, 2019, approved Senate Bill 778 extends the training deadline set in Senate Bill 1343 from January 1, 2020 to January 1, 2021. The changes made by SB 778 not only extends the due date to January 1, 2021, but also addresses concerns about supervisory employees and clarifies when temporary workers must be trained. Read about these changes here.

Ensuring the Training is in Compliance

In order for the Sexual Harassment and Abusive Conduct Prevention training to be compliant, it must meet the following requirements. The training must:

Be administered in a classroom setting, through interactive E-learning, or through a live webinar. E-learning training must provide instructions on how to contact a trainer who can answer questions within two business days.

Be conducted by an eligible trainer:

Attorneys who have been members of the bar of any state for at least two years and whose practice includes employment law under the Fair Employment and Housing Act or Title VII of the federal Civil Rights Act of 1964;

Human resource professionals or harassment prevention consultants with at least two years of practical experience in:

Designing or conducting training on discrimination, retaliation, and sexual harassment prevention;

Responding to sexual harassment or other discrimination complaints;

Investigating sexual harassment complaints; or

Advising employers or employees about discrimination, retaliation, and sexual harassment prevention.

Law school, college, or university instructors with a post-graduate degree or California teaching credential and either 20 hours of instruction about employment law under the FEHA or Title VII.

Explain the following topics:

The definition of sexual harassment under the Fair Employment and Housing Act and Title VII of the federal Civil Rights Act of 1964;

The statutes and case-law prohibiting and preventing sexual harassment;

The types of conduct that can be sexual harassment;

The remedies available for victims of sexual harassment;

Strategies to prevent sexual harassment;

Supervisors’ obligation to report harassment;

Practical examples of harassment;

The limited confidentiality of the complaint process;

Resources for victims of sexual harassment, including to whom they should report it;

How employers must correct harassing behavior;

What to do if a supervisor is personally accused of harassment;

The elements of an effective anti-harassment policy and how to use it;

“Abusive conduct” under Government Code section 12950.1, subdivision (g)(2).

Discuss harassment based on gender identity, gender expression, and sexual orientation, which shall include practical examples inclusive of harassment based on gender identity, gender expression, and sexual orientation.

Include questions that assess learning, skill-building activities to assess understanding and application of content, and hypothetical scenarios about harassment with discussion questions.

SB 1343 compliant trainings will be made available later this year via the California Department of Fair Employment and Housing (DFEH) website. However, employers can hire eligible qualified trainers to conduct the trainings at their convenience.

The DFEH has made available a sexual harassment and abusive conduct prevention toolkit, that includes a sample Sexual Harassment and Abusive Conduct Prevention training, certificate of completion and other resources for employers to use in conjunction with an eligible trainer.

Other training options include the online Anti-Harassment training Rancho Mesa offers to all of its clients’ supervisors and employees throughout the country in response to California’s Senate Bill 1343 (SB 1343) and Senate Bill 1300 (SB 1300).

For questions about this training requirement or to learn how to enroll your supervisors and employees, register for the “How to Enroll Supervisors and Employees in the Online Anti-Harassment Training” webinar or contact Rancho Mesa’s Client Services Department at (619) 438-6869.

Rancho Mesa Insurance will continue to monitor training options as they become available.

Why Would a Contractor Purchase Employment Practices Liability Insurance?

Author, Kevin Howard, CRIS, Account Executive, Construction Gorup, Rancho Mesa Insurance Services, Inc.

Insurance is often considered a necessary evil by business owners. It can represent a significant line item on a profit & loss statement rivaling the cost in some cases of payroll, material costs and rent. With deductibles that can range from $15,000-$25,000 per claim, why then would a business spend dollars on an insurance policy that is not required by either state law or part of any General Contractor’s insurance specifications?

Author, Kevin Howard, CRIS, Account Executive, Construction Group, Rancho Mesa Insurance Services, Inc.

Insurance is often considered a necessary evil by business owners. It can represent a significant line item on a profit & loss statement rivaling the cost in some cases of payroll, material costs and rent. With deductibles that can range from $15,000-$25,000 per claim, why then would a business spend dollars on an insurance policy that is not required by either state law or part of any general contractor’s insurance specifications?

What does an EPLI policy cover?

Employment Practices Liability Insurance (EPLI) policies typically extend coverage to the following:

Wrongful termination of an employee who alleges violation of their contract;

Sexual harassment claims by one employee against another;

Wage related claims by employees who allege denial of overtime pay or tips, or working “off the books." Note: Most carriers offer a defense only sub limit for this type of claim;

Claims of unequal or unfair pay between employees performing the same job and having similar skills, education, seniority and responsibility;

Discrimination claims based on age, race, gender or sexual orientation;

Third Party. Example: Your employee out in the field of work upsets another subcontractor’s employee, a customer at their home, a student at a school enough to where they file a lawsuit against you.

Why do businesses resist purchasing EPLI?

Declining to purchase EPLI can stem from businesses feeling that they are not large enough for this type of claim to occur. Many owners have close relationships with their employees and never believe any of the above scenarios could occur within their organization. And yet, many more can assume that a General Liability policy would cover these types of potential claims when, in fact, most have specific EPLI exclusions. This type of thinking could result in losses that have severe financial consequences for your company. Let’s take a quick look at three common EPLI exposures facing the construction industry.

Common EPLI Claims in the Construction Industry

Rapid growth and layoffs are unique aspects of the construction industry that can cause the elimination of a specific position and/or termination. With these ebbs and flows, contractors unintentionally open themselves up to wrongful termination cases which can carry into discrimination charges, as well. It can also be common to see employees bring post-employment wage & hour claims, which center around improper overtime, breaks, etc. Lastly, contractors' work very often involves interaction and exposure to the public. This interaction can lead to comments, inferences, or specific actions that non-employees find offensive. Claims brought by these third parties are difficult to prove when the employer is unable to witness the events first-hand.

Light Bulb Moment

In these and other potential claim scenarios, employers without EPLI must outlay their own funds to find legal representation and fight the charges. Legal costs add up quickly regardless of the documentation an employer has kept on file and the conviction they have that an employee’s claim is frivolous. Defending yourself in today’s environment can become cost ineffective very quickly. Light bulb moments can occur when EPLI limits are unavailable because coverage is not in force and an owner is staring at a “balance sheet loss,” resulting in a six figure settlement.

Consult Your Broker for EPLI Options

At Rancho Mesa, as it relates to coverage for our clients, we often say "you would rather be looking at it than for it”. That is, you want to be looking at a policy that will respond to coverage than for one at the time of a loss. Take time to explore the nuances of employment practices liability insurance with a knowledgeable broker. Allow an expert to educate you on the real exposure to your company, ask to spreadsheet different policy forms, deductibles and limits in an effort to balance the annual premium with the potential impact of a large loss.

For more information about Employment Practices Liability Insurance, contact Rancho Mesa Insurance at (619) 937-0164.